Paid Family Leave

How is it Reported on a Tax Return?

An analyst reached out to us recently on the Bukers Hotline with a question about the Family and Medical Leave Act (FMLA) and how it may affect their borrower’s cash flow. The borrower told the analyst that their W-2 wages were going to appear lower than expected on Page 1 of their tax return, but in reality, their salary remained consistent to historical performance. The analyst asked us, “how could this be possible?” Let’s help them out on this week’s cash flow article.

Paid Family Leave - State Intervention

Did you know that more and more states are starting to adopt policies that mandate paid family leave for employees? Let’s back up for a second. The federal law for family and medical leave (under the FMLA) is that employers must allow employees up to 12 weeks of unpaid leave per year to allow for bonding time with newborns or being a caregiver for a family member with a serious medical issue. This law mandates companies to continue these individuals’ health insurance policies and ensures that their positions will remain unfilled during this time.

Certain states have intervened and added another clause to this federal policy which also mandates that employees continue to receive salaries, or at least a portion thereof, during this family leave period. These are considered “Mandatory Participation” states, including Washington, New York, California, Oregon, and others. For states with mandatory paid family leave, employees and employers have a portion of their wages withheld each pay period that goes towards funding this state program. When employees take their family leave, they continue to earn a salary, except it is paid by the state rather than the employer.

So how does it cash flow? What adjustments should we make?

Well, in short, this continues to cash flow the same as it normally would. The borrower still receives their entire salary, it just comes from two different sources – the state government pays them for up to 12 weeks of the year, and their employer pays them for the rest of the year. For cash flow analysis, we simply need to know where to look in our borrower’s documentation to substantiate the flow of cash to the individual. The portion of salary paid by their employer will continue to be reported in Box 1 of the borrower’s W-2, which will then flow to Line 1a on Form 1040. Nothing new so far.

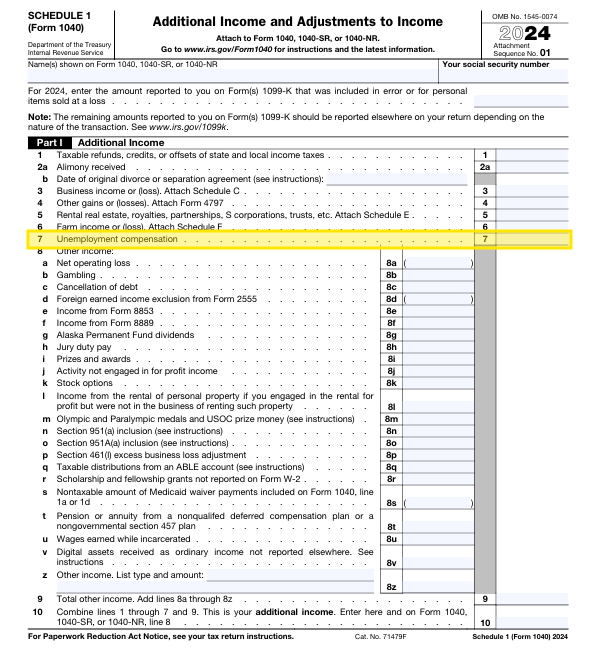

The portion of salary paid to the borrower from the government (pursuant to the state’s rules on FMLA) may be reported on a Form 1099-G issued to the borrower. From there, it will likely flow to Form 1040, Schedule 1, Line 7 – Unemployment compensation. State rules vary, so you may alternatively see this amount reported on Schedule 1, Line 8 – Other income. For cash flow purposes, we can consider that amount to be a component of salaries and wages and ensure that it is added to our borrower’s cash flow.

Voluntary Participation States

There are a handful of other states that have adopted similar policies designed to ensure that employees continue to earn their wages during family leave, however it is paid from a participating insurance company rather than the state itself. These are considered “Voluntary Participation” states and include Tennessee, Texas, and Florida, amongst others.

The cash flow implications for these states would be similar to mandatory participant states, except the family leave portion of wages is coming from the insurance company rather than the state government. Because of this, the borrower will not receive a Form 1099-G. Be on the lookout for alternative forms of documentation, such as a Form 1099 or equivalent, issued by the private insurer to the borrower.

Best Practices

So, what are our key takeaways? First off, as an analyst, ensure that you are taking into account all of the facts and circumstances of a borrower’s day-to-day life. If they recently had a child, take a minute to consider that they may have received state benefits via paid family leave. If their W-2 wages for the year seem lower than historical average, you may want to ask them if they received a Form 1099-G, and you can also keep a lookout for unemployment compensation to be reported on Schedule 1 of Form 1040. In some cases, your borrower may not know to give you a heads up of the paid family leave, so understanding the different ways income flows to a borrower’s tax return is crucial in arriving at the most accurate cash flow figure.

If your institution uses the Bukers software and you ever come across a difficult tax return spreading dilemma, feel free to call the Bukers Hotline at 503-520-1303. Our team of CPAs is standing by and ready to help work through any tax return question you may have while performing cash flow analysis.