Tax-Exempt Interest Income from Pass-Through Entitles

Have you ever encountered an unusually large dollar amount on an individual’s tax return that made you stop and think twice? Recently, an analyst had this situation occur and called in to the Buker’s Hotline for assistance. On this month’s cash flow article, let’s explore their scenario and the appropriate cash-flow adjustments required.

Unusual Tax-Exempt Interest Income

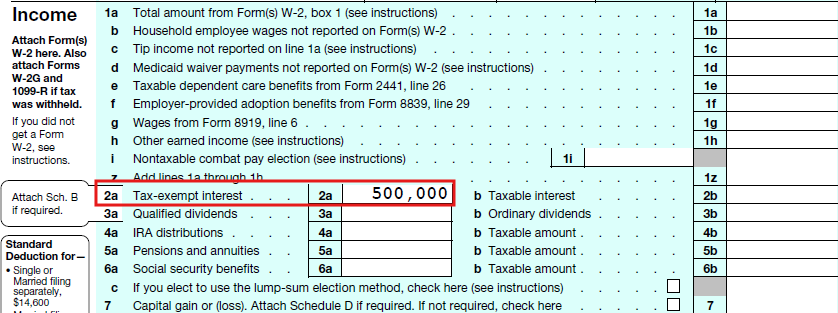

The analyst explained that their borrower reported over $500,000 of tax-exempt interest income on line 2a on their Form 1040. Their tax return did not have much other activity, and prior years’ returns did not show similar amounts of tax-exempt interest income. To make things worse, since tax-exempt interest income is not listed on Schedule B, the analyst had no clue where this large potential cash inflow was coming from. The analyst’s perspective was understandable – they felt that the $500,000 of tax-exempt interest income seemed random, as if it came from nowhere. Without the historical support, the analyst felt this potential cash inflow raised some red flags worth investigating.

Support Found on Schedule K-1

To make sense of this situation, we looked to see if there were any supporting statements related to the significant tax-exempt interest income reported on the tax return. Since tax-exempt interest income is not reported on Schedule B, we had to find alternative sources of documentation to learn more. As luck would have it, there was a supporting schedule attached to the end of the return that broke down the total interest income reported by the individual during the year. We were able to see on that schedule that the tax-exempt interest income was actually passing through to the borrower’s return from their Form 1065 Schedule K-1.

The income was earned by the borrower’s partnership and passed through to the individual’s return based on their ownership percentage of the partnership entity. This means that the $500,000 of tax-exempt interest income was pass-through income that was being reported on the individual’s return for tax purposes only. More importantly for our cash flow analysis, that tax-exempt interest income represents “paper income” that we do not include in our borrower’s cash flow figures.

Pass-Through Income/Loss comes in all shapes and sizes!

This unusual example of high tax-exempt interest income is a great reminder that items of pass-through income and loss can come in many different forms. Typically, tax-exempt interest income is related to an individual’s holdings of municipal bonds or other tax-exempt investments. In this case, the borrower had no historical precedent for such a high figure for tax-exempt interest income, so it made sense that this was being passed through by the borrower’s partnership.

We don’t typically think of tax-exempt income being an item that would be passed through by a partnership or S Corporation, but it is certainly possible. The analyst was correct to say that “something felt off” regarding the large tax-exempt interest income. The extra steps we took ensured they did not erroneously overstate the borrower’s cash flow available to service debt.

If you are a Bukers software user and you ever come across a similar situation where you, as the analyst, feel as if something doesn’t quite feel right with the borrower’s tax return, feel free to call the Bukers Hotline. Our team of CPAs is ready and happy to help you with any questions that may arise within the spreading process.